Over the past few years, financial institutions have made meaningful investments in credit engagement and have built strong strategies to support it. Across digital banking platforms, many have introduced tools that give users access to their credit scores and reports. They’ve added alerts, educational content, and insights designed to help customers and members better understand and manage their financial health. These are important advancements, and they reflect a broader industry commitment to improving both engagement and financial well-being. The capability is there. What’s missing is reach.

Opt-in models limit how far credit engagement can scale. Even well-designed credit tools tend to reach only a portion of the digital user base. Activity is strong among those who opt in, but participation across the broader customer population remains uneven. This showcases that the ceiling is the enrollment model, not the effort.

This isn’t unique to banking. Across digital experiences more broadly, opt-in participation often falls well below full reach. When engagement depends on users taking the first step, many simply never do.

The result is untapped potential and it raises an important question:

How can institutions make it easier for customers and members to engage from the very start?

The hidden constraint of opt-in enrollment

In most digital banking environments today, credit engagement tools are available, but they rely on users to take the first step.

That typically means customers and members must:

- Discover the feature within the experience

- Make an active decision to enroll

- Return independently to continue engaging

This model works well for motivated users. But across any customer base, there will always be a range of behaviors, priorities, and levels of financial awareness. Even when the value is obvious, many customers or members don’t engage simply because the experience requires them to go get it.

That’s a limitation of the model, not the institution.

But availability alone doesn’t always translate into broad, sustained engagement.

When engagement is concentrated within a subset of users, it can create downstream challenges:

- Limited visibility into the full customer base

- Missed opportunities to engage earlier in the credit journey

- Difficulty aligning offers with real-time needs

For financial institutions focused on growth, these gaps matter. Not because the strategy is flawed, but because its reach is inherently constrained.

A shift toward embedded engagement

As digital banking experiences continue to evolve, many institutions are exploring ways to reduce friction and make engagement more seamless from the outset.

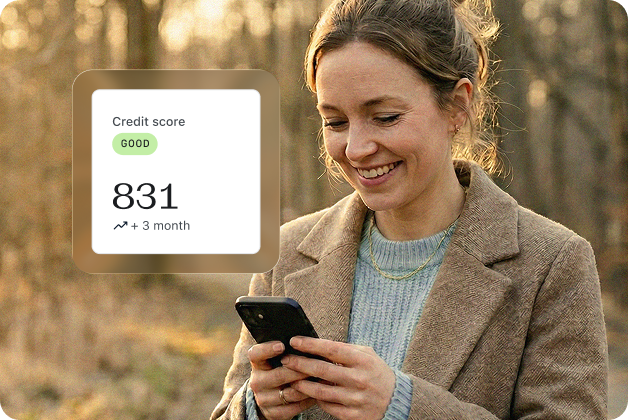

One approach gaining traction is embedded credit engagement, where access to credit information is integrated directly into the core digital banking experience rather than positioned as an optional feature.

Solutions like SavvyMoney InstantAccess, when embedded within the Candescent Intelligent Banking platform, are designed to address this challenge by reducing enrollment friction and expanding access. Instead of requiring users to opt in through a separate process, eligible users can engage directly within the digital banking experience, with terms accepted naturally in context.

While the impact of this shift is subtle at the surface, it’s meaningful in practice. It transforms credit engagement from something customers and members must initiate to something they can simply experience.

From episodic checks to a full-base view

When access is embedded and immediate, credit engagement becomes a more natural part of how customers and members interact with their finances. Instead of checking a score once and disengaging, they gain ongoing visibility within an environment they already use regularly. Over time, this creates a more consistent connection to their credit health.

For institutions, that translates to:

- More frequent interaction with credit insights

- Greater awareness of financial behaviors and trends

- A stronger foundation for long-term engagement

This isn’t about increasing activity for its own sake. Instead. it’s about making engagement easier, more intuitive, and more sustainable.

One of the most important advantages of broader engagement is the quality of insight it enables. In an opt-in environment, the data generated through credit tools reflects only those who have actively chosen to participate. This group is often more financially engaged than the broader population, which can unintentionally skew perspective.

With more inclusive enrollment, institutions gain clearer visibility into credit behavior across a wider portion of their digital audience.

That expanded visibility allows for:

- Earlier identification of trends

- More accurate segmentation

- Better alignment between customer conditions and institutional strategies

Rather than operating from a partial view, decision-makers can work with a more complete understanding of their customers and members’ financial realities.

Aligning engagement with real-time customer needs

Another meaningful shift occurs in how institutions approach outreach and lending. Traditional engagement strategies often rely on campaign cycles—planned outreach based on predefined segments. While effective in certain contexts, campaigns don’t always align with real-time customer needs.

A customer or member’s readiness to borrow is often shaped by dynamic factors:

- Changes in their credit profile

- Improvements in financial position

- Moments of need that arise unexpectedly

When engagement is continuous and visibility is broader, financial institutions are better positioned to recognize and respond to these moments. Solutions like SavvyMoney InstantAccess support this approach by enabling personalized, pre-qualified offers based on current credit conditions—bringing timing and relevance closer together.

The focus shifts from “when to market” to “when the customer is ready.”

Unlocking growth within the digital experience

As these elements come together—embedded access, continuous engagement, broader data visibility, and real-time relevance—the role of digital banking begins to evolve.

What has traditionally been viewed as a service channel becomes a more active contributor to growth.

Institutions can begin to see:

- Increased application activity driven by higher engagement

- Improved alignment between offers and eligibility

- More efficient conversion when timing and relevance are optimized

Importantly, this growth doesn’t rely on new channels or increased acquisition spend. It comes from more fully activating the relationships institutions already have.

Why now

The pressure to deepen relationships and drive growth efficiently continues to grow.

At the same time, customer expectations are evolving. Experiences in other industries have set a high bar for simplicity, personalization, immediacy and zero friction. Financial institutions are responding, but the challenge isn’t just delivering more functionality. It’s ensuring that functionality is experienced consistently and at scale.

The financial institutions pulling ahead are not necessarily those with the most features. They are the ones that have focused on how those features are introduced and integrated into the daily customer experience.

They are:

- Reducing friction wherever possible

- Embedding value directly into existing workflows

- Prioritizing access and visibility from the very first interaction

The path forward: expanding the reach of your credit engagement strategy

Credit engagement strategies across the industry are stronger than ever in both capability and intent. The opportunity now is to ensure those strategies reach as much of the customer base as possible.

For many institutions, that means looking beyond the tools themselves and focusing on how customers and members experience them from the start.

Increasingly, this involves a shift from:

- Optional experiences → to more seamlessly embedded ones

- Occasional interactions → to continuous engagement

- Partial visibility → to a more complete understanding of the customer base

When engagement becomes easier to access and simpler to maintain, institutions are better positioned to deliver both customer value and measurable growth.

If opt-in is capping how far your credit strategy reaches, the highest-leverage move isn’t a new tool. It’s changing how customers and members can meet the one you already have.